2022

Fellow Partners,

Ouch. 2022 was a brutal year for many in capital markets and certainly for our partnership.

Your Q4 2022 statements and our annual audit will be released shortly. Check these for specifics — they vary only by the timing of your joining the partnership.

Business performance

The most important question we ask and answer each year is: how did our businesses perform?

Most of our businesses had a good year:

Revenue grew an average of 17%. 11 businesses had double-digit growth, three had single-digit growth, and two had single-digit declines.

All but three businesses were free cash flow positive, had years of cash on their balance sheet, or had positive adjusted margins (with reasonable adjustments), indicating that these businesses will not be reliant on capital markets for continued funding. Most had several of these attributes.

Four businesses bought back their own shares, and eight businesses had directors using personal funds to buy shares in the open market.

In general, we own businesses with secular tailwinds, operating leverage, low churn, and strong balance sheets.

For our digital assets, despite a year of horrendous events in the space:

Demand continues to grow. The number of holders, active participants, active developers, and decentralized infrastructure all grew through 2022.

Supply continues to decline. Fewer tokens are being issued and less of the circulating supply is being traded than at any point in these assets’ brief history.

Overall, market conditions have incentivized better behavior and many bad actors, bad businesses, and bad ideas are being washed out of the market. This pulling of the weeds will benefit those growing real plants.

Our actions

How did we respond to this business performance?

We started and ended the year with 18 investments. We added one new position, exited one position, and made few other changes aside from increasing the size of several of our positions as they became more affordable relative to our estimates of their long-term intrinsic value.

As I have said in prior writings, a highlight of the year was the majority of partners increasing their investments in the fund. That allowed us to increase the size of our positions at favorable prices. That also enabled a type of efficiency I love — no one paid this partnership to sit on cash. This "storing cash with LPs" reduces my fee income (and hence is less common), but it is a fairer way to operate.

Events of the year also helped validate the software-style alpha, beta, full-release approach we have taken to growing our partnership. 2020 was our alpha release. The evolutions we made in 2021 were our beta release. We will have a “version 1” launch shortly. We’ve done this for two reasons:

As often discussed, signaling to and selecting only the right partners is both the biggest risk and biggest opportunity for us to build an enduring, high-trust partnership. We continue to improve our ability to do so, and this is in part due to the fact that we have chosen to do it slowly.

We expect continued improvement of our process, including our ability to identify the best opportunities, scale into them, and manage the positions. A "raise and go" approach is antithetical to the time and experience required for positive evolution. Again, slow, intentional growth is the best path.

Fund performance

If our businesses had a relatively good year and our partnership was stable and growing, why did our fund have such a bad year?

Ben Graham noted that the market is a voting machine in the short-term and a weighing machine in the long-term. There was a lot of voting going on in 2021 and 2022 and much less weighing. We are a partnership that wants to be weighed, and over the long-term, we will be.

The reality of 2022 proved to be one of “nowhere to hide”. Bonds had their worst year on record. Stocks, too, had a rough year. The lack of dispersion in outcomes was surprising. Defense and commodities firms (generally outside our circle of competence) had good years driven by war and energy shortages. Some traders and market makers (not our strategy) had great years driven by market volatility. Beyond this, high-or-low multiple growth, high-or-low quality value…just about everything got hammered. Macro factors overwhelmed business-level factors.

Let’s examine the major factors and consider whether they are likely to permanently impair our capital.

In Seasons Pt. 1: A Better Mental Model we noted that markets and businesses are best understood through the lens of seasons as opposed to artificial increments of time such as months and quarters. In Seasons Pt. 2: How We Got Here we noted that an excess of excesses including easy money, maximum globalization, and geopolitical stability led to asset booms, and that this season has turned. Here’s the summary:

In Seasons Pt. 3: Direction of Travel we noted that we are likely to normalize back to longer-term trends. Money will have a modest cost (that is, risk will be priced), and globalization and geopolitical stability will retreat from their zeniths but remain beneficial. These normalizations, which negatively impact prices, will eventually be balanced by increased resilience and reduced risk, which positively impact prices.

This will take time.

I recently spoke with a 20-year veteran of the world’s largest appliance manufacturer (Bosch). Pre-pandemic they manufactured 160,000 dishwashers per month. Today — still — that number is just 90,000 per month, a 44% decline. The culprit? A Wi-Fi chip used in many of their appliances that is only manufactured in a single location in Shanghai. Rolling lockdowns in China dramatically slowed chip production, limiting their ability to finish appliances.

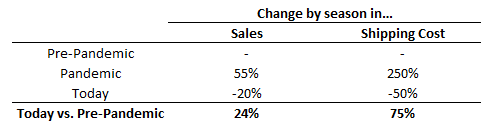

Similarly, a major furniture manufacturer who supplies Wayfair, Restoration Hardware and other brands recently noted the difference in their sales vs. shipping cost over the past few years:

How does one optimize their businesses amidst these realities? They don’t. But they can and will as more predictability returns.

We already see evidence of improvement.

The world’s largest car manufacturer is once again producing a record number of vehicles.

Shipping has also improved dramatically:

And Bosch? China opening up is helping in the short-term. Longer-term they’ve learned a bigger lesson on supply chain resilience, are in-sourcing their chip production, and building a second chip manufacturing plant in Malaysia.

These types of adaptation are upsides of chaos that lead to increased resilience and reduced risk.

On jobs — the biggest component of the current economic equation — evidence suggests the labor market may be less tight than we think. If true, this will flow through over the coming months and support normalization of price inflation.

, Steven J. Davis, et al.")

Zooming out, the long-term trends of progress are powerful. Despite the present headwinds, far more value will be created in the next decade than in the last, and this partnership will be part of it.

Equally, the long-term cost of capital has been on a relentless decline for centuries, and while “free” is absolutely the wrong interest rate, we do not have good reasons to believe that the normalized cost of capital will be enormously high — that would counteract most of the data we have on the subject, and the efficiencies that led to its multi-century decline.

The takeaway for long-term, patient capital such as ours is that our investments in progress remain reasonable ones, provided one underwrites assuming a reasonable cost of capital (as we do).

Our concentrated portfolio paired with our minimal trading activity guarantees substantial price volatility throughout our journey, but the major factor of permanent relevance remain business performance throughout our period of investment. This remains our focus.

Lessons learned

Mistakes often come from overweighting apparent short-term wins, without fully recognizing the consequent, long-term costs. Not investing for the future is a form of this.

The Berkshire Hathaway annual meetings always open with video clips from the firm's history. In one, Warren Buffett is asked how he differs from other investors. "Patience" is his one-word answer. Our patience has been tested this year (and possibly for a number of future years; we'll see). But our focus is unchanged.

However, if we could play 2022 over, I would make two changes.

The first would be more patience in deploying additional capital. We are never trying to bottom-tick the market, but when the balance of price-accretive vs. price-destructive variables is clearly tilted one way, more patience is warranted. While I remain convinced that we will be envious of the prices at which we purchased assets in 2022, no rush was needed. I am generally optimistic, but a slower pace of capital deployment amidst the sea of bad news (and there has been plenty) would have benefitted us.

The second would be increased caution around businesses that may be dependent on capital markets for further funding. We have three holdings today that have less runway than I would like and difficult paths to operating profitability. While they’re far from dead, I generally dislike any variable that could require a company to raise capital — the worst time to raise money is when you need it — and the perception of these three positions is that they will. The game is far from over; we’ll see.

Zooming out, the world is ruled by power laws. Our purpose is to catch them and hang on to them when we do. Our work continues.

In closing

If you read nothing else in this letter, know that we do not rely on ultra-low interest rates for successful outcomes. Our focus and patience permits an investment strategy that is likely to out-perform as the market rises, and under-perform as the market declines, as we’ve already seen in the short 30 months of this partnership. In the long-run we care little about short-term performance vs. the market. If we’ve found good investments and hold onto them, their value when we sell will be all that matters.

The majority of my family’s net worth is in this partnership. I feel every percentage point and, since inception, have constructed our partnership such that I will feel the worst financial pain should our capital be permanently impaired. That’s only fair (though rather uncommon in this business).

Thank you for the continued opportunity to compound trust with you.

As always, please reach out any time.

All the best,

John

Founder and Managing Partner