Fellow Partners,

A warm welcome to four new partners!

Thank you for the connections you have been making to other parties who share our long-term, patient, focused values.

If this letter has been forwarded to you and you would like to discuss further, please reach out to info@phronesisfund.com.

Here is the November update.

Summary

Learn the building blocks (in rock and roll and investing)

Forward-looking market returns are not mouth watering…

…but we only need to invest in a few great businesses for satisfactory returns in the long-run

Leading companies will dominate via extreme scale or defending a niche

We figure out what a business is worth and pay a lot less

The real money is made in the waiting

Learn the building blocks

Investor letters need more wisdom from the world of music (and more rock and roll). Here’s a great example:

For everything you learn, learn the thing that is the building block for the thing you just learned…trace back why you like the thing, and learn the thing that made the thing you like, and you will be five times better every time you do that.

John Mayer

This is how to learn to think from first principles and a route we regularly follow when applying practical wisdom to crafting the Phronesis Fund. It is the reason I expect this partnership to be good and to get better. We think from first principles — and much of that is intentionally standing on the shoulders of many others that came before us.

A corollary that is not celebrated nearly enough: in the past decade the sum of human knowledge has been put on the internet. What amazing opportunities this creates. We’re still in the early innings of seeing what this enables.

Here is the full the clip and some good riffs (4 minutes):

Where is the market now?

We are in a very low interest rate environment which has the following properties:

Anything involving financing has become more attractive since money is less expensive (e.g. record bond issuance and record home buying and refinancing)

The future earnings power of companies has become more valuable because the discount rate is lower (e.g. today’s value of $100 of earnings in 2030 is $39 with a 10% discount rate, $61 with a 5% discount rate, or $100 with a 0% discount rate)

Returns demanded by investors for all asset classes are reduced, leading to higher valuations for companies (e.g. on many metrics such as price/sales Apple stock is now more expensive than at any other point in its history). The Fed’s asset buying also juices valuations.

All these factors encourage risky behavior and “reaching” for return

Ramifications of fiscal and monetary policy are summarized nicely in this chart, and in great detail in Jesse Livermore’s epic piece on upside-down markets (60+ min read).

Howard Mark’s latest memo (30 min read) summarizes the market implications:

…the odds aren’t on the investor’s side, and the market is vulnerable to negative surprises. This is how I described the prior years, and I’m back to saying it again. The case isn’t extreme — prices aren’t grievously high (assuming interest rates stay low, which they’re likely to do for several years). But it’s hard in this context to find anything mouth-watering.

Howard Marks, October 2020

In short, prospective returns across asset classes are lower.

We only need a few great companies

But take heart. This is a major reason we don’t believe in blindly buying the market and hoping it goes up.

We only need to invest in a few great companies to produce good (and potentially great) results.

The great personal fortunes in the country weren't built on a portfolio of fifty companies. They were built by someone who identified one wonderful business.

Warren Buffett

I frequently return to this sentiment. At every point in the years I have followed the market I could find strongly negative, scary sentiment, alongside businesses that knocked the cover off the ball. Of course the real challenge is finding those businesses and holding on.

But this is worth pondering, particularly as the market climbs its classic wall of worry.

We are not trying to buy the market (if you are, please go buy our benchmark or something similar). We are trying to buy a few great companies and let them be great for years on end.

I recently came across one of the most interesting questions I’ve seen in years: who is more likely to default, Amazon or the US Government?

Ignoring the bit about the government being able to print unlimited money to stave off default, the sentiment is fascinating: some businesses are so good they have become (or are becoming) something truly outstanding, to the benefit of many including us, their shareholders.

That’s where we plan to be.

And on another bright note, check out the recent spike in applications to open businesses:

Who will survive? Who will thrive?

Thinking at the level of individual businesses requires a framework for understanding the sorting and shifting that we are observing day to day. I encountered one of the most useful through Josh Wolfe (Lux Capital) and Daniel Ek (Spotify):

Businesses will trend towards dominance via extreme scale or a defensible niche.

These 12 words explain an enormous amount of the change we are seeing around us. As we’ve dealt with the realities of Covid-19, Amazon, Target, Costco and other mega-scale players have dominated retail. Netflix, Disney, Nintendo and other mega-scale players have dominated entertainment. The Visa / Mastercard electronic payment duopoly has accelerated.

By contrast, in the long-term the local barber, great chefs, high quality local clubs and communities are in no danger (though I feel for them in the short-term). Geography and other scale-limiting factors create defensible niches that can be won with quality.

We should be cautious about investing in businesses that do not fit either of these categories. They are likely to struggle.

When do we buy?

When we find great businesses able to dominate via extreme scale or defensible niche, when should we buy? Doubtless you’ve seen comparisons of when-to-buy-what across investing styles. A recent interview with Joel Greenblatt (45 min read) phrased our thinking nicely:

I gave a speech last year called “Is Value Investing Dead?” and my answer was “yes, no, maybe, and I don’t care.” And the reason for that is it really depends on how you define value. If you define it like Russell or Morningstar as low price/book or low price/sales its had a tough time. [By these definitions] in the last five years growth has outperformed value by 11 percent per year. In the last 12 months it’s about 43 percent….

…If you define value like we do, which is to figure out what a business is worth and pay a lot less — that’s what I define as value investing (Ben Graham would say leave a large margin of safety) — then that’s never really going to go out of style. We look at companies like we’re a private equity firm. No private equity firm buys a business because it’s a low price/book or low price/sales. They’re really looking at cash flows.

Joel Greenblatt, October 2020

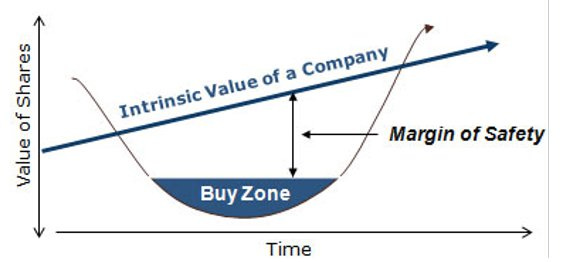

Here’s the idea as a visual:

Closely connected to buying businesses with a margin of safety is buying businesses that can produce exceptional returns on incrementally invested capital — a key component of intrinsic value.

I’m going be long…CEOs that can invest all the money they make today for the future simply because I can now lazily let that person work on my behalf.

Chamath Palihapitiya

A great example: Amazon has invested the money made in web services and e-commerce to build another Fortune 50 company within itself: Amazon Logistics.

While generating a relatively small amount of press, Amazon Logistics was launched in 2014, delivered about 20% of Amazon packages in 2018, and grew that to nearly 50% in 2019, for a 2019 total of 3.5 billion packages delivered (vs. 3.9 billion for FedEx, 5.5 billion for UPS, and 6.2 billion for the USPS). The scale and speed of that growth is mind boggling. Within 10 years of its launch Amazon logistics will likely eclipse its primary competitors in package volume.

How did they do it? Check out their latest earnings release (screenshot below). While revenue and earnings (net income) are always the focus of headlines, Amazon lists these last. The first half of the information they report is about cash flow. Why? Amazon obsessively uses their cash flow from existing businesses to reinvest in those businesses and build out new businesses. Their target is not profit — it is using cash flow from things they built to build even more.

The long-term advantages of Amazon Logistics are substantial. Their focus on cash flow as opposed to net income is the type of thinking that enables such massive scale investments that ultimately create long-term advantages.

Another favorite example is Costco who provide a textbook model of wise capital allocation. When they can put capital to use at high rates of return they build more warehouse stores and invest to grow these stores. When they can’t, they pay a dividend, and occasionally a special dividend to return larger amounts of cash to shareholders.

Costco’s sales per warehouse report (below, and in each annual report) provides a good high-level lens on this, and an impressive degree of transparency to shareholders. This is an easy way to see Costco’s track record of building and investing in stores when, on average, those stores can grow over time. When opportunities aren’t sufficiently attractive, Costco returns capital to shareholders that can be invested in more attractive opportunities.

If all this all sounds like common sense — it is. But very, very few companies behave this way. The incentives for executives to build empires are often too great. However, you will find many of the happy few mature capital allocators in our portfolio.

When do we sell?

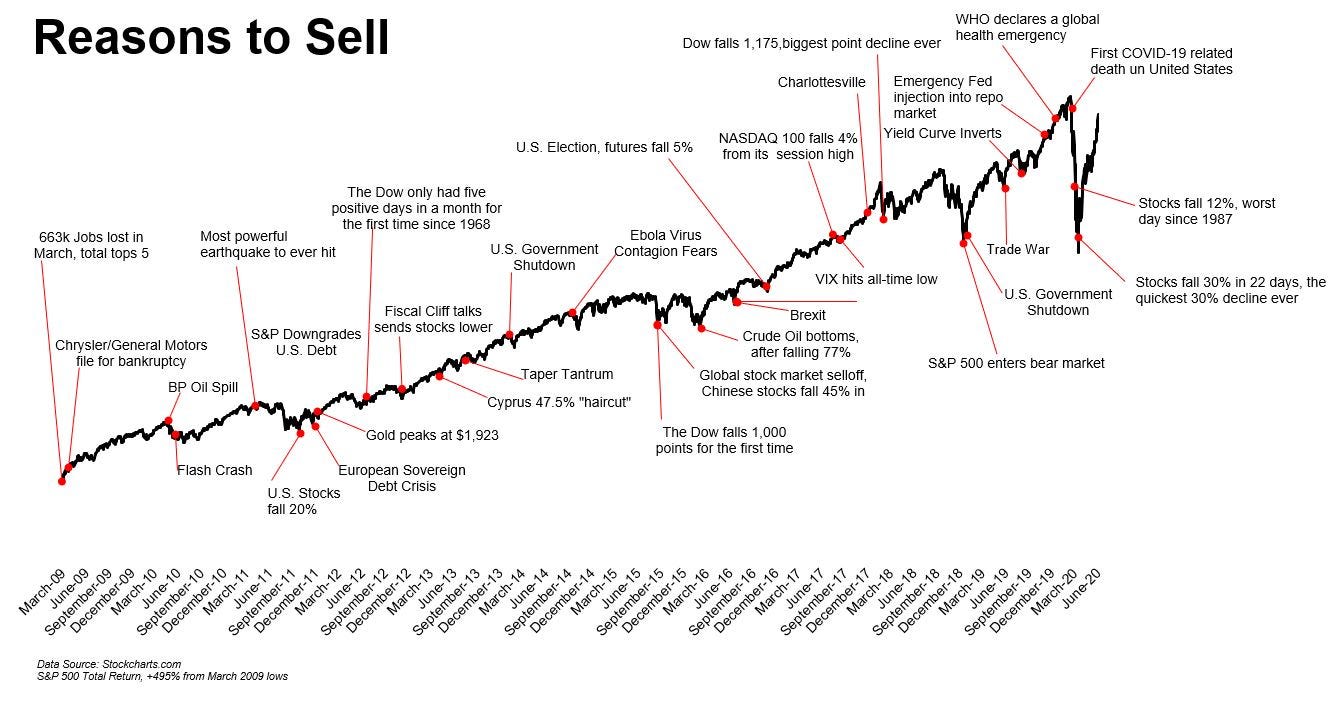

There are always reasons to sell.

The astute observer notes the general trend, and takes heart that our strategy net of fees has outperformed the trend since its inception five years ago.

This isn’t to say there are never reasons to sell. We do sell — we just have a very high bar for doing so. The reason must be extremely compelling. The overall calculus is fairly simple:

Business quality or performance has substantially deteriorated

Substantially higher-quality opportunities exist — but these must be so much better that we can afford to take the transaction costs and tax hit that comes with selling and still believe we will outperform over the long-run by trading up

Here’s an example.

Portfolio company Costco is a wonderful business. Portfolio company Booking Holdings is also a wonderful business.

During the depths of market despair over coronavirus Costco was very well positioned — a fiercely loyal customer base, warehouse-style stores for buying en masse, substantial price advantages, and growing online distribution to name a few. Booking Holdings, at first glance, was poorly positioned — its major sources of revenue are from the travel industry. But, due to good positioning, Costco’s stock price was about even on the year. Booking Holdings was down about 40%. Some basic logic told us that (1) Booking Holdings was well positioned to weather the storm and potentially emerge stronger, and (2) even if the travel industry took 2-4 years to recover to pre-Covid levels, Booking Holdings’ intrinsic value should only be down 10-15%, not the 40% reduction it was trading at.

So what did we do? We sold some Costco and bought some Booking Holdings. We remain proud owners of both companies. But over the next 2-4 years I suspect Booking Holdings will outperform Costco simply because both are wonderful businesses but Booking Holding’s setup was substantially better.

Statements, focus, and patience

The stock market is a device to transfer money from the impatient to the patient.

Warren Buffett

Quarterly statements arrived in your inboxes early last month. You will also shortly receive an email from the Fund’s administrator with signup details to a portal that allows you to see the performance of your positions in the fund on-demand.

I encourage you to review your positions in the fund any time you wish. I also encourage you to be thoughtful about how often you review them. There is a mountain of research that tells us excessive information leads to excessive action, and this is especially true in long-term investing.

In the long-run investors get the returns they deserve, and an enormous component of successful long-term investing is the ability to be patient and focus on owning wonderful businesses while ignoring what the crowd thinks. Market values will jump around. We solely focus on the value of our positions over a period of years.

The big money is made not in the buying and selling, but in the waiting.

Unknown

If we own wonderful businesses over the long-term we will be very pleased with the resulting performance.

Closing items

I have begun aggregating partner resources on this page for ease of access. Think of this as a one-stop-shop with links to all the resources available to you.

As always, please feel free to reach out to discuss the above or anything else.

All the best,

John

Founder and Managing Partner